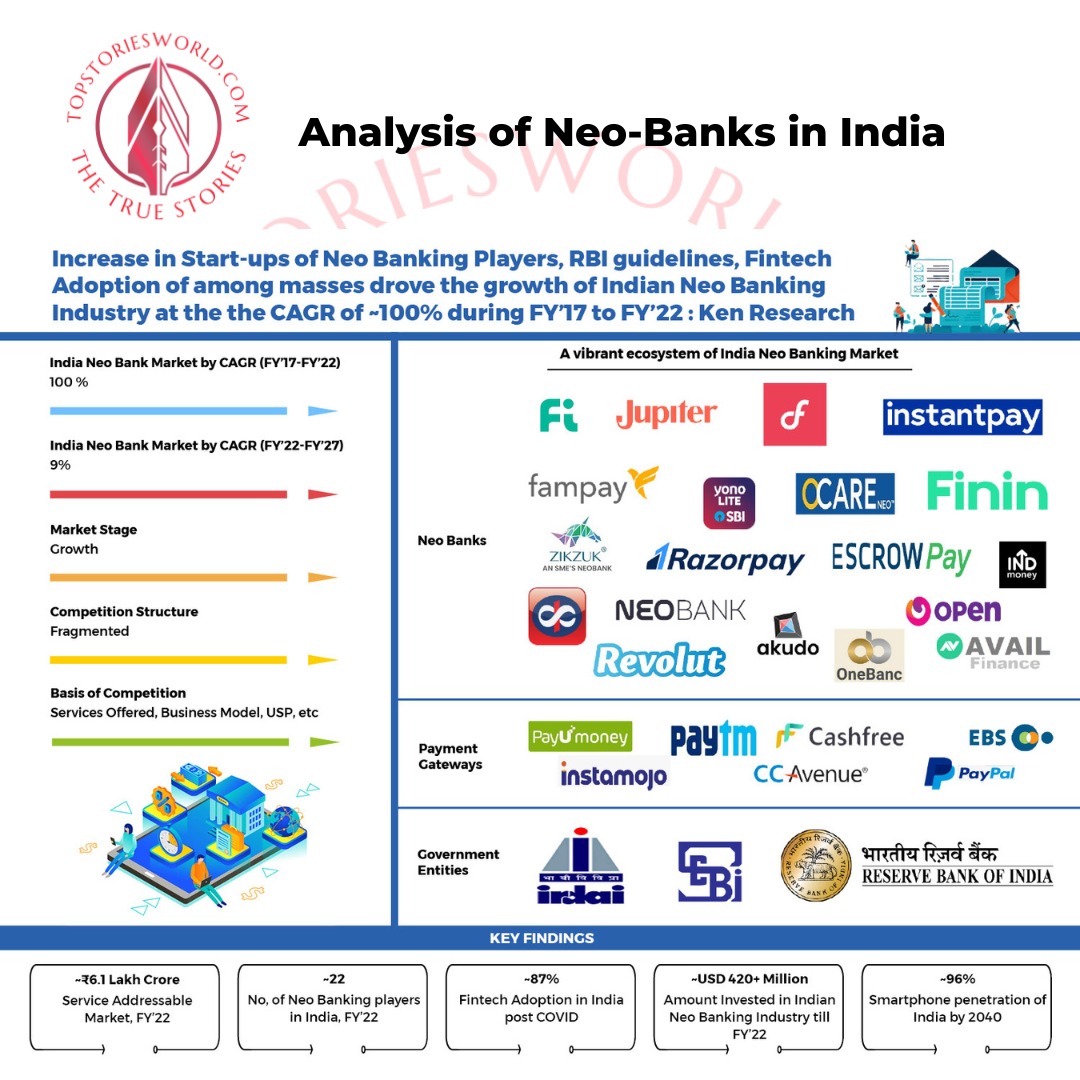

Analysis of Neo-Banks in India Posted on January 15, 2023 News By Akta Yadav 227 Views Analysis of Neo-Banks in India Neo-banks, also known as digital or online-only banks, are shaking up the traditional banking industry with their innovative approach to offering financial services. With the primary function of offering customers a tech-led banking experience, they provide access to funds for lending and even hold customers' funds. They distribute products through an app and ensure customer satisfaction, end-to-end customer acquisition, and client retention. But what sets neo-banks apart from traditional banks is their unique ability to disrupt the status quo. They are not restrained by legacy systems or complex regulations, allowing them to offer low-cost models and a customer-centric experience. This has made them popular among India's underserved Micro, Small and Medium Enterprises (MSME) sectors. Benefits of Neo Banks in India One of the critical advantages of neo-banks in India is that they add an experiential layer to traditional banking, making it possible to access financial products that are not readily available to the 600 million Indians and the 65 million MSMEs. Neo-banks can improve digital distribution channels and onboarding for customers by leveraging the success of the India FinTech stack, such as Digi locker, Aadhaar, UPI 2.0, and the account aggregator model. Some of the critical benefits of neo-banks in India include the following: Convenience: Neo-banks operate entirely online, allowing customers to access banking services 24/7 from anywhere with an internet connection. This eliminates the need to visit physical branches, saving customers time and effort. Low-cost models: Neo-banks are not constrained by the legacy systems and complex regulations that traditional banks are, allowing them to offer low-cost models and more affordable banking services. Customised experience: Neo-banks use advanced technology, such as AI and big data, to provide customers with a personalised and customised banking experience. This allows them to offer tailored financial services and products to meet the specific needs of different customer segments. Faster onboarding: Neo-banks use digital platforms and streamlined processes to onboard new customers quickly and efficiently. This makes it easy for customers to open an account and use banking services without requiring long wait times or extensive paperwork. Access to underserved MSME sector: Neo-banks has had a major part in serving the needs of India's underserved Micro, Small and Medium Enterprises (MSME) sector. A 2019 report by the Reserve Bank of India (RBI) estimated the credit gap for this sector to be at a staggering INR 20-25 trillion. Neo-banks have made this sector their targeted market by offering them banking services that traditional banks cannot provide. The value proposition of neo-banks in India is centred around catering to the underserved Micro, Small and Medium Enterprises (MSME) sector. A 2019 report by the Reserve Bank of India (RBI) estimated the credit gap at a staggering INR 20-25 trillion. Recognising this gap, neo-banks have made this sector their targeted market by offering them banking services that traditional banks have yet to offer safely and effectively on a digital platform. In addition to catering to the MSME sector, neo-banks have attracted capital due to their revolutionary capabilities and out of the box approach to the way financial services are offered. For example, a UK-based neo-bank became the most valuable fintech firm at ~USD30 billion as of 2021, as it raised USD750+ million for product development and expansion. Regulations of Neo Banks However, neo-banks in India currently operate in a regulatory vacuum as they are not directly regulated by the Reserve Bank of India (RBI). One way that neo-banks are addressing this regulatory predicament is by outsourcing their banking responsibilities to regulated banks, creating strategic partnerships with traditional banks, and providing amplified services on behalf of existing ones. This model is already being used worldwide by some of the biggest names in neo-banking. Banks must adhere to and impose stringent outsourcing obligations when partnering with neo-banks. Another approach neo-banks in India take acting as business correspondents (BCs) of traditional banks. These companies are expected to have widespread retail outlets. However, RBI does not recognise virtual banks entirely and does not regulate neo-banks. Conclusion In conclusion, neo-banks in India is a growing trend driven by the fact that traditional banks cannot effectively and safely offer their services on a digital platform. Neo-banks are expected to become even more popular as technology improves. Neo-banks can be differentiated from traditional banks in several ways, and regulatory and policy developments around neo-banks in India are also evolving.

Australia surpasses West Indies in main record list and chases Pakistan's all-time record following historic victory News February 6, 2024

But what sets neo-banks apart from traditional banks is their unique ability to disrupt the status quo. They are not restrained by legacy systems or complex regulations, allowing them to offer low-cost models and a customer-centric experience. This has made them popular among India's underserved Micro, Small and Medium Enterprises (MSME) sectors.

But what sets neo-banks apart from traditional banks is their unique ability to disrupt the status quo. They are not restrained by legacy systems or complex regulations, allowing them to offer low-cost models and a customer-centric experience. This has made them popular among India's underserved Micro, Small and Medium Enterprises (MSME) sectors.